Understanding Credit

Find a Co-Signer

A parent, a guardian, or a close relative might be an individual who can co-sign on a small

loan for you. By getting a co-signer, the financial institution knows that if you can't make

your payments then the person who co-signed becomes responsible for the payment(s).

Opening a Bank Account

After opening the bank account and having it for several months, the financial institution

can look at your account to see that you have an income flow coming into your account.

They might be willing to offer you a credit card with a low limit on it. Talk to your bank

representative when you open a bank account.

Secured Credit Cards

Secured credit cards require a cash deposit and then you can make monthly payments for

purchases, thus establishing credit.

Student Credit Cards

Financial institutions entice students to use their services by offering low credit limit on

the use of the credit card, but with higher interest rates because the student who has no

credit is a higher risk for them. If you use your credit card to try to establish credit,

remember it is your payments on time that matter most.

Auto Loan

Some used car dealerships will help you finance your car with a larger down payment to

customers who don't have a credit history. In many states if you even miss just one

payment, creditors will contact you with a notification of "right to cure." This means if

you miss a payment, the financial institution has a right to repossess the automobile.

A parent, a guardian, or a close relative might be an individual who can co-sign on a small

loan for you. By getting a co-signer, the financial institution knows that if you can't make

your payments then the person who co-signed becomes responsible for the payment(s).

Opening a Bank Account

After opening the bank account and having it for several months, the financial institution

can look at your account to see that you have an income flow coming into your account.

They might be willing to offer you a credit card with a low limit on it. Talk to your bank

representative when you open a bank account.

Secured Credit Cards

Secured credit cards require a cash deposit and then you can make monthly payments for

purchases, thus establishing credit.

Student Credit Cards

Financial institutions entice students to use their services by offering low credit limit on

the use of the credit card, but with higher interest rates because the student who has no

credit is a higher risk for them. If you use your credit card to try to establish credit,

remember it is your payments on time that matter most.

Auto Loan

Some used car dealerships will help you finance your car with a larger down payment to

customers who don't have a credit history. In many states if you even miss just one

payment, creditors will contact you with a notification of "right to cure." This means if

you miss a payment, the financial institution has a right to repossess the automobile.

A little while after you have established credit, you will have a credit score.

The three major credit bureaus are:

Equifax - www.equifax.com

P.O. Box 740241

Atlanta, GA 30374-0241

1-800-685-1111

Experian - www.experian.com

P.O. Box 2104

Allen, TX 75013-0949

1-888-EXPERIAN (397-3742)

TransUnion - www.transunion.com

P.O. Box 1000

Chester, PA 19022

1-800-916-8800

These organizations gather consumer credit information and then sell this information

to other businesses (credit report). Once you have established some credit, each of

these major credit bureaus will have a FICO score for you.

(NOTE: FICO is not a credit bureau; FICO is the score you receive from a credit bureau.)

The three major credit bureaus are:

Equifax - www.equifax.com

P.O. Box 740241

Atlanta, GA 30374-0241

1-800-685-1111

Experian - www.experian.com

P.O. Box 2104

Allen, TX 75013-0949

1-888-EXPERIAN (397-3742)

TransUnion - www.transunion.com

P.O. Box 1000

Chester, PA 19022

1-800-916-8800

These organizations gather consumer credit information and then sell this information

to other businesses (credit report). Once you have established some credit, each of

these major credit bureaus will have a FICO score for you.

(NOTE: FICO is not a credit bureau; FICO is the score you receive from a credit bureau.)

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

According to the Fair Isaac Corporation that calculates the popular “FICO score,"

the following factors (and weighting) determine your credit score.

• Payment History (35%) -- includes account payment information, bankruptcy

or judgments, how long overdue payments are, amount past due, and the time since

any adverse occurrences.

• Amounts Owed (30%) -- includes the amounts owed on accounts individually and

totaled together as a whole,number of accounts with balances, proportion of

credit line used and proportion of installment loan amounts still owed.

• Length of Credit History (15%) -- includes the time since you accounts have been

open as well as the time since your accounts have been active.

• New Credit (10%) -- includes the number of and time since recently opened accounts

and proportion to total accounts, number of and time since recent credit inquires,

and the re-establishment of positive credit history following past payment problems.

• Types of Credit Used (10%) -- includes the number of various types of accounts,

like credit cards, retail accounts, installment loans, mortgage, etc.

the following factors (and weighting) determine your credit score.

• Payment History (35%) -- includes account payment information, bankruptcy

or judgments, how long overdue payments are, amount past due, and the time since

any adverse occurrences.

• Amounts Owed (30%) -- includes the amounts owed on accounts individually and

totaled together as a whole,number of accounts with balances, proportion of

credit line used and proportion of installment loan amounts still owed.

• Length of Credit History (15%) -- includes the time since you accounts have been

open as well as the time since your accounts have been active.

• New Credit (10%) -- includes the number of and time since recently opened accounts

and proportion to total accounts, number of and time since recent credit inquires,

and the re-establishment of positive credit history following past payment problems.

• Types of Credit Used (10%) -- includes the number of various types of accounts,

like credit cards, retail accounts, installment loans, mortgage, etc.

Investopedia defines bank credit as "an agreement between banks and borrowers where

banks trust a borrower to repay funds plus interest for either a loan, credit card or line of

credit at a later date."

To get credit, you have to have a credit history. What? That's right. If you don't have a

credit history, then you can't get credit.

So what are some ways to get credit without having a credit history?

banks trust a borrower to repay funds plus interest for either a loan, credit card or line of

credit at a later date."

To get credit, you have to have a credit history. What? That's right. If you don't have a

credit history, then you can't get credit.

So what are some ways to get credit without having a credit history?

Several Methods of Establishing Credit (according to Debt.org)

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

The Three Major Credit Bureaus

How is Your FICO Score Calculated?

Figuring Your FICO Score (Estimation Calculators)

Credit Card Minimum Payment Calculator)

Credit card debt occurs for one reason and one reason only. You don't pay your credit

card balance offwhen the bill comes due. Any time you do not pay off your credit card

balance, you credit card debt.

Paying the MINIMUM amount due each month only allows you to continue to use your

credit card. What this does, though, is put you into credit card debt.

Play with the calculator below (from bankrate.com) and see how much you owe your

financial institutionbecause you decide to pay only the MINIMUM amount due.

card balance offwhen the bill comes due. Any time you do not pay off your credit card

balance, you credit card debt.

Paying the MINIMUM amount due each month only allows you to continue to use your

credit card. What this does, though, is put you into credit card debt.

Play with the calculator below (from bankrate.com) and see how much you owe your

financial institutionbecause you decide to pay only the MINIMUM amount due.

Final Note

Credit is NOT money. If a credit card were money, it would be called a money card.

Credit is given to you with a promise that you will pay back the borrowed amount

some time in the future. Credit is a way topurchase something today that you can pay

for some time in the future.

As you can see from the calculator above, you get yourself into credit trouble when

you don't make your full monthly payments each month.

Using credit for long-term purchases (house, automobile, education) has advantages.

When you pay off your house and automobile, you then truly own your house and car.

If you don't make your payments on your house or automobile, the financial institution

can foreclose on your house or repossess your car.

Your student loan for an education is an investment into your perceived future earnings.

Credit is given to you with a promise that you will pay back the borrowed amount

some time in the future. Credit is a way topurchase something today that you can pay

for some time in the future.

As you can see from the calculator above, you get yourself into credit trouble when

you don't make your full monthly payments each month.

Using credit for long-term purchases (house, automobile, education) has advantages.

When you pay off your house and automobile, you then truly own your house and car.

If you don't make your payments on your house or automobile, the financial institution

can foreclose on your house or repossess your car.

Your student loan for an education is an investment into your perceived future earnings.

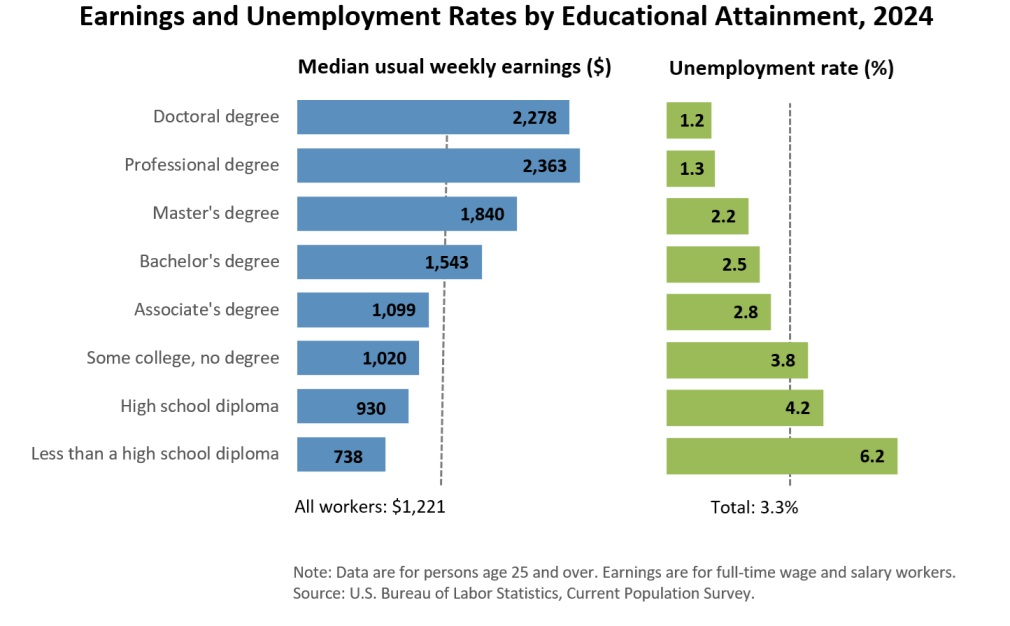

Using the calculator above,

figure the median YEARLY

earnings of each of the degree

attainments shown on the

Bureau of Labor Statistic graph

to the left by multiplying the

Median usual weekly earnings

times 52 weeks.

figure the median YEARLY

earnings of each of the degree

attainments shown on the

Bureau of Labor Statistic graph

to the left by multiplying the

Median usual weekly earnings

times 52 weeks.

The graph above shows the unemployment rate by degree attainment and median usual weekly

earnings by degree attainment. To attain higher degrees you must make yourself worse off in

the short run (giving up earnings today to get a degree) to make yourself better off in the long run

(future employment and future earnings).

If you take out a student loan for your education, make sure you work harder than you have ever

worked in your entire life and attain that degree. To take out a student loan and quit school a

year or two later can be a poor investment on borrowed money.

Best of luck making the right decisions on when and how to borrow money, but most importantly

pay off your debts before you retire. Life becomes a lot easier during your retirement years when

you have no debt.

earnings by degree attainment. To attain higher degrees you must make yourself worse off in

the short run (giving up earnings today to get a degree) to make yourself better off in the long run

(future employment and future earnings).

If you take out a student loan for your education, make sure you work harder than you have ever

worked in your entire life and attain that degree. To take out a student loan and quit school a

year or two later can be a poor investment on borrowed money.

Best of luck making the right decisions on when and how to borrow money, but most importantly

pay off your debts before you retire. Life becomes a lot easier during your retirement years when

you have no debt.

| Steven M. Reff Economics Lecturer University of Arizona (2007 - 2016) The 2015 University of Arizona Five-Star Faculty Award |

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

My FICO Score:

https://www.myfico.com/fico-credit-score-estimator/estimator

https://www.myfico.com/fico-credit-score-estimator/estimator

Calcxml -- What is My Credit Score?

https://www.calcxml.com/calculators/credit-score-calculator-new

https://www.calcxml.com/calculators/credit-score-calculator-new

Simon Fitzgerald LLC -- Credit Score Calculator--What is My Credit Score?

https://www.simonfitzgerald.com/credit-score-calculator/

https://www.simonfitzgerald.com/credit-score-calculator/

Use one of the links below to help you understand how your credit score is calculated.

Because you are a young student, it might be difficult to come up with a correct credit

score for you, but it will give you a heads up on how important your credit score will

become when you start borrowing for a car, a home, or other assets you want to purchase

later in your life.

NOTE: Do NOT click on other links found inside these websites as these websites

should only be used to calculate your credit score.

Because you are a young student, it might be difficult to come up with a correct credit

score for you, but it will give you a heads up on how important your credit score will

become when you start borrowing for a car, a home, or other assets you want to purchase

later in your life.

NOTE: Do NOT click on other links found inside these websites as these websites

should only be used to calculate your credit score.

Click on this link: Bank.com