Purchasing Insurance

Located to the right are all the

different types of insurance that can

be purchased according to Wikipedia.

However, many people tend to have

just a couple or a few different

insurance policies.

different types of insurance that can

be purchased according to Wikipedia.

However, many people tend to have

just a couple or a few different

insurance policies.

When you are young and just starting out, your first insurance policy will probably be auto insurance.

1. Determine your state's minimum insurance requirements.

2. Consider your own financial situation in relation to the required insurance and consider whether you need to

increase your limits to protect your assets.

3. Review the status of your driving record — do you have any outstanding tickets or points on your driver's license?

4. Check your current coverage to find out how much you are paying.

5. Get competing quotes from insurance companies a month before your annual policy is about to expire.

6. Make follow-up phone calls to insurance companies to get additional information about coverage.

7. Inquire about discounts.

8. Evaluate the reliability of the insurance companies you're considering by visiting your state's insurance

department website, reviewing consumer surveys and talking to family and friends.

9. Review the policy before finalizing it.

10. Remember to cancel your old policy if you already have one.

1. Determine your state's minimum insurance requirements.

2. Consider your own financial situation in relation to the required insurance and consider whether you need to

increase your limits to protect your assets.

3. Review the status of your driving record — do you have any outstanding tickets or points on your driver's license?

4. Check your current coverage to find out how much you are paying.

5. Get competing quotes from insurance companies a month before your annual policy is about to expire.

6. Make follow-up phone calls to insurance companies to get additional information about coverage.

7. Inquire about discounts.

8. Evaluate the reliability of the insurance companies you're considering by visiting your state's insurance

department website, reviewing consumer surveys and talking to family and friends.

9. Review the policy before finalizing it.

10. Remember to cancel your old policy if you already have one.

Auto Insurance

The different types of coverage you can obtain when purchasing automobile insurance are:

*LIABILITY COVERAGE (automobile and bodily injury) which is mandatory in most states.

*UNINSURED AND UNDERINSURED MOTORIST COVERAGE helps pay medical bills in case a driver with no insurance hits you.

*COMPREHENSIVE COVERAGE may help cover damage to your car from things like theft, fire, hail or vandalism.

*COLLISION COVERAGE helps if you're involved in an accident with another vehicle

*LIABILITY COVERAGE (automobile and bodily injury) which is mandatory in most states.

*UNINSURED AND UNDERINSURED MOTORIST COVERAGE helps pay medical bills in case a driver with no insurance hits you.

*COMPREHENSIVE COVERAGE may help cover damage to your car from things like theft, fire, hail or vandalism.

*COLLISION COVERAGE helps if you're involved in an accident with another vehicle

When you purchase auto insurance it typically is stated with three numbers.

For instance, if you purchase a 25/50/25 policy, the first number represents the highest amount your insurance

company will pay per injured person ($25,000), the second number represents the highest total amount your insurance

company will pay for the accident ($50,000), and the third number represents the maximum amount the insurance

company will pay for property damage ($25,000).

A policy that states 100/300/100 means $100,000 per person; $300,000 total; and $100,000 property damage.

You don't want to be over insured because it means you are paying too much for insurance you don't need and you

don't want to be under insured as you will be liable for physical or bodily damages above what your insurance covers.

Check with your insurance agent to make sure you are properly insured.

For instance, if you purchase a 25/50/25 policy, the first number represents the highest amount your insurance

company will pay per injured person ($25,000), the second number represents the highest total amount your insurance

company will pay for the accident ($50,000), and the third number represents the maximum amount the insurance

company will pay for property damage ($25,000).

A policy that states 100/300/100 means $100,000 per person; $300,000 total; and $100,000 property damage.

You don't want to be over insured because it means you are paying too much for insurance you don't need and you

don't want to be under insured as you will be liable for physical or bodily damages above what your insurance covers.

Check with your insurance agent to make sure you are properly insured.

When you move out of your parent's house, your next insurance you might purchase is renter's insurance.

Most renter's insurance policies include four basic types of coverage:

PERSONAL PROPERTY (stolen items, windstorm or fire damage)

LIABILITY (guest getting injured in your home or your dog biting a someone)

Note that some insurers exclude certain dog breeds from coverage.

MEDICAL PAYMENTS (pays for a guest’s injuries on your property without requiring a lawsuit)

LOSS OF USE (pays out if you need to relocate while your home or apartment is undergoing repairs after a disaster)

Most renter's insurance policies include four basic types of coverage:

PERSONAL PROPERTY (stolen items, windstorm or fire damage)

LIABILITY (guest getting injured in your home or your dog biting a someone)

Note that some insurers exclude certain dog breeds from coverage.

MEDICAL PAYMENTS (pays for a guest’s injuries on your property without requiring a lawsuit)

LOSS OF USE (pays out if you need to relocate while your home or apartment is undergoing repairs after a disaster)

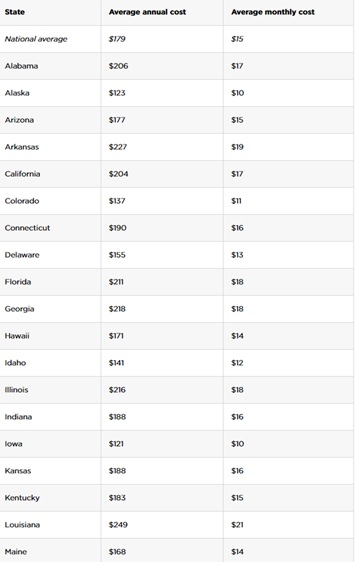

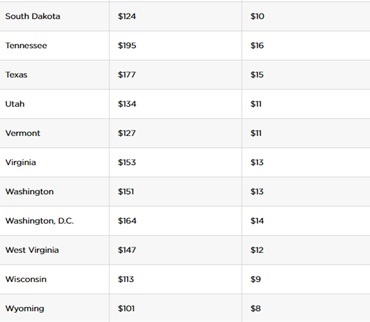

Renter's Insurance

To the right find your state's

average annual and monthly cost

of renter's insurance in your state

to give you a rough idea on what

you will pay for renter's insurance.

The cost of your renter's

insurance is dependent upon

a few categories:

Where you live.

Your previous claims.

Your credit history.

Your dog.

Your coverage limits.

Your deductible.

average annual and monthly cost

of renter's insurance in your state

to give you a rough idea on what

you will pay for renter's insurance.

The cost of your renter's

insurance is dependent upon

a few categories:

Where you live.

Your previous claims.

Your credit history.

Your dog.

Your coverage limits.

Your deductible.

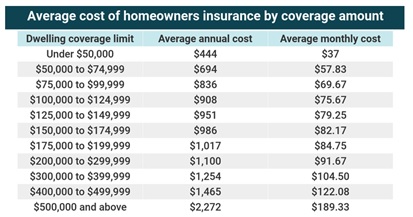

Homeowner's insurance is usually tied in

with your mortgage payment (principal +

interest + real estate taxes + homeowner's

insurance) and varies in price based upon

several factors. Here are some factors that

can help you reduce your homeowner's

insurance.

1. Raise your deductible

2. Make your home more secure

3. Don't file small claims

4. Ask about lesser-known discounts

5. Account for home improvements

6. Bundle your auto and home insurance

7. Build your credit score

8. Shop around

with your mortgage payment (principal +

interest + real estate taxes + homeowner's

insurance) and varies in price based upon

several factors. Here are some factors that

can help you reduce your homeowner's

insurance.

1. Raise your deductible

2. Make your home more secure

3. Don't file small claims

4. Ask about lesser-known discounts

5. Account for home improvements

6. Bundle your auto and home insurance

7. Build your credit score

8. Shop around

Homeowner's Insurance

This is where purchasing insurance gets a little tricky. You will most likely be contacted by a life insurance

agent during your lifetime. Here is a list of the different types of life insurance policies.

Term life insurance

Whole life insurance

Universal life insurance

Indexed universal life insurance

Variable life insurance

Variable universal life insurance

Final expense insurance

Group life insurance

Which one do you choose? That's up to you. Do an Internet search on the pros and cons of each policy

to see which policy suits you best.

agent during your lifetime. Here is a list of the different types of life insurance policies.

Term life insurance

Whole life insurance

Universal life insurance

Indexed universal life insurance

Variable life insurance

Variable universal life insurance

Final expense insurance

Group life insurance

Which one do you choose? That's up to you. Do an Internet search on the pros and cons of each policy

to see which policy suits you best.

Life Insurance

| Steven M. Reff Economics Lecturer University of Arizona (2007 - 2016) The 2015 University of Arizona Five-Star Faculty Award |