| The Federal Open Market Committee (FOMC) that meets 8 times each year. Remember this Committee also includes the members of the Board of Governors. |

| The Board of Governors meet every other Monday. |

The interest rate on reserve balances (IORB rate) and the primary

credit rate (formerly known as the discount rate) are determined

by the FRB). IORB is the primary tool for the Federal Reserve's

monetary policy.

credit rate (formerly known as the discount rate) are determined

by the FRB). IORB is the primary tool for the Federal Reserve's

monetary policy.

The maximum number of governors who sit on The Board of

Governors of the Federal Reserve is 7 governors.

Notice above as of February 13, 2023 the Board had the maximum

number.

The members of the Board of Governors of the Federal Reserve

System are nominated by the President and confirmed

by the Senate. A full term is 14 years.

The Chair and the Vice Chair of the Board, as well as the Vice

Chair for Supervision, are nominated by the President from among

the members and are confirmed by the Senate. They serve a term

of four years.

Governors of the Federal Reserve is 7 governors.

Notice above as of February 13, 2023 the Board had the maximum

number.

The members of the Board of Governors of the Federal Reserve

System are nominated by the President and confirmed

by the Senate. A full term is 14 years.

The Chair and the Vice Chair of the Board, as well as the Vice

Chair for Supervision, are nominated by the President from among

the members and are confirmed by the Senate. They serve a term

of four years.

The maximum number of members who sit on the Federal Open

Market Committee (FOMC) consists of 12 members. Notice above

that the FOMC had this maximum number as of February 13:

7 members of the Board of Governors of the Federal Reserve

System as of February 13, 2023.

1 President of the Federal Reserve Bank of New York always

sits on the FOMC

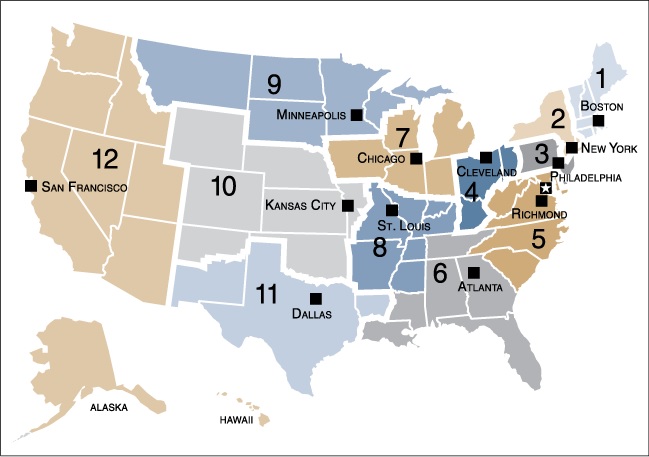

4 of the remaining eleven Reserve Bank presidents, who serve

one-year terms on a rotating basis. (See district bank map below)

Market Committee (FOMC) consists of 12 members. Notice above

that the FOMC had this maximum number as of February 13:

7 members of the Board of Governors of the Federal Reserve

System as of February 13, 2023.

1 President of the Federal Reserve Bank of New York always

sits on the FOMC

4 of the remaining eleven Reserve Bank presidents, who serve

one-year terms on a rotating basis. (See district bank map below)

12 Federal Reserve District Bank Presidents

The New York Federal Reserve District Bank President and

4 Federal Reserve District Bank Presidents sit on the

Federal Open Market Committee (FOMC)

The remaining 7 Federal Reserve Bank Presidents attend

the FOMC meetings and bring their district board reports

to help advise The Board of Governors on the

Primary Credit Rate (formerly entitled the Discount Rate)

that should be administered. The Board of Governors

then makes the final decision on this rate.

The New York Federal Reserve District Bank President and

4 Federal Reserve District Bank Presidents sit on the

Federal Open Market Committee (FOMC)

The remaining 7 Federal Reserve Bank Presidents attend

the FOMC meetings and bring their district board reports

to help advise The Board of Governors on the

Primary Credit Rate (formerly entitled the Discount Rate)

that should be administered. The Board of Governors

then makes the final decision on this rate.

2023 Board of Governors of the Federal Reserve System (FRB)

• Jerome H. Powell, Board of Governors, Chair

• Michael S. Barr, Board of Governors, Vice Chair for Supervision

• Michelle W. Bowman, Board of Governors

• Lael Brainard, Board of Governors, Vice Chair

(resigned on February 14, 2023 to become the Director of the

National Economic Council at the White House)

• Lisa D. Cook, Board of Governors

• Philip N. Jefferson, Board of Governors

• Christopher J. Waller, Board of Governors

• Jerome H. Powell, Board of Governors, Chair

• Michael S. Barr, Board of Governors, Vice Chair for Supervision

• Michelle W. Bowman, Board of Governors

• Lael Brainard, Board of Governors, Vice Chair

(resigned on February 14, 2023 to become the Director of the

National Economic Council at the White House)

• Lisa D. Cook, Board of Governors

• Philip N. Jefferson, Board of Governors

• Christopher J. Waller, Board of Governors

The History of Ample Reserves Along with Everything Your Students Have to Know about Ample

Reserves for the May 2024 Exam in Conjunction with FEE.org:

https://reffonomics.com/firesidechatamplereserves.html

What is Covered on the May Exam in Macroeconomics?

https://reffonomics.com/amplereservesregime2023.html

AP Macroeconomics Lesson for BOTH Money Market and Ample Reserves Graphs

https://reffonomics.com/fed2023.html

Cell Phone Graphing Ample Reserves:

https://reffonomics.com/graphsmac4a.html

Reserves for the May 2024 Exam in Conjunction with FEE.org:

https://reffonomics.com/firesidechatamplereserves.html

What is Covered on the May Exam in Macroeconomics?

https://reffonomics.com/amplereservesregime2023.html

AP Macroeconomics Lesson for BOTH Money Market and Ample Reserves Graphs

https://reffonomics.com/fed2023.html

Cell Phone Graphing Ample Reserves:

https://reffonomics.com/graphsmac4a.html

| The Federal Open Market Committee (FOMC), the Board of Governors, and the 12 District Bank Presidents |

2023 Federal Open Market Committee (FOMC) Committee Members

• Jerome H. Powell, Board of Governors, Chair

• Michael S. Barr, Board of Governors

• Michelle W. Bowman, Board of Governors

• Lael Brainard, Board of Governors (resigned February 14)

• Lisa D. Cook, Board of Governors

• Philip N. Jefferson, Board of Governors

• Christopher J. Waller, Board of Governors

• John C. Williams, New York, Vice Chair

• James Bullard, St. Louis

• Susan M. Collins, Boston

• Esther L. George, Kansas City

• Loretta J. Mester, Cleveland

• Jerome H. Powell, Board of Governors, Chair

• Michael S. Barr, Board of Governors

• Michelle W. Bowman, Board of Governors

• Lael Brainard, Board of Governors (resigned February 14)

• Lisa D. Cook, Board of Governors

• Philip N. Jefferson, Board of Governors

• Christopher J. Waller, Board of Governors

• John C. Williams, New York, Vice Chair

• James Bullard, St. Louis

• Susan M. Collins, Boston

• Esther L. George, Kansas City

• Loretta J. Mester, Cleveland

| 2019 (January) |

| Monetary Policy -- Ample Reserves Regime is Here to Stay |

The Board of Governors of the Federal Reserve System and the Federal Open

Market Committee (FOMC) shall maintain long-run growth of the monetary and

credit totals proportionate with the economy's long-run potential to increase

production, so as to promote effectively the goals of:

Maximum Employment

Stable Prices

Moderate Long-Term Interest Rates

The "Dual Mandate" is to maintain Maximum Employment and Stable Prices.

Market Committee (FOMC) shall maintain long-run growth of the monetary and

credit totals proportionate with the economy's long-run potential to increase

production, so as to promote effectively the goals of:

Maximum Employment

Stable Prices

Moderate Long-Term Interest Rates

The "Dual Mandate" is to maintain Maximum Employment and Stable Prices.

On the Dual Mandate Bullseye below, shown on the y axis is the inflation rate determined by the Personal Consumption

Expenditure Index, an inflation index used by the Federal Reserve. The targeted inflation rate by the FOMC is 2% (stable

prices). Shown on the x axis is the unemployment rate. The bullseye indicates where the Natural Rate of Unemployment

(maximum employment) lies at a certain period of time.

Expenditure Index, an inflation index used by the Federal Reserve. The targeted inflation rate by the FOMC is 2% (stable

prices). Shown on the x axis is the unemployment rate. The bullseye indicates where the Natural Rate of Unemployment

(maximum employment) lies at a certain period of time.

| To use the interactive Dual Mandate Bullseye follow the directions underneath the graph. |

| 1977 (November) |

| The Federal Reserve Act of 1977 (Dual Mandate) |

| The Present (10 minutes) |

| The REFF® and FRED® Graphs |

| The REFF® AR Graph |

| Money Market Graph Rip It Out! Simple Money Multiplier (1/RR) Rip It Out! |

| next to a FRED® graph. |

PL

PLc

"Effective July 27, 2023, the Federal Open Market Committee (FOMC) directs the Desk to:

Undertake open market operations as necessary to maintain the federal funds rate in a target range of 5-1/4 to 5-1/2 percent.

Undertake open market operations as necessary to maintain the federal funds rate in a target range of 5-1/4 to 5-1/2 percent.

PLf

When the FOMC raises the target range, banks increase their

lending rates for borrowers (including other banks), making

credit more expensive and savings accounts more lucrative.

Undertake open market operations as necessary to maintain

the Federal Funds Rate in a target range of 5-1/4 to 5-1/2

percent.

The Federal Funds Rate is a POLICY RATE. It is the

rate that banks charge other banks for borrowing overnight.

lending rates for borrowers (including other banks), making

credit more expensive and savings accounts more lucrative.

Undertake open market operations as necessary to maintain

the Federal Funds Rate in a target range of 5-1/4 to 5-1/2

percent.

The Federal Funds Rate is a POLICY RATE. It is the

rate that banks charge other banks for borrowing overnight.

| Teach the Differences Among |

PL

| The Future (30 minutes) |

| The Money Supply -- Rip It Out! |

Administered Rate #1: "The Board of Governors of the Federal Reserve System voted unanimously to raise the

Interest Rate on Reserve Balances (IOR) to 5.4 percent, effective July 27, 2023."

Interest Rate on Reserve Balances (IOR) to 5.4 percent, effective July 27, 2023."

i

The Policy Rate is the Federal Funds Rate.

i1

Shown below are 3 Administered Rates that influence the Policy Rate (Federal Funds Rate) to remain

within the target range.

within the target range.

i1

Administered Rate #3: "The FOMC directs the desk to: Conduct standing Overnight Reverse Repurchase Agreement (ON RRP)

operations at an offering rate of 5.3 percent and with a per-counterparty limit of $160 billion per day."

operations at an offering rate of 5.3 percent and with a per-counterparty limit of $160 billion per day."

| February 2021 Senate Banking Committee on the Semiannual Monetary Policy Report |

up

Administered Rate #2: "In a related action, the Board of Governors of the Federal Reserve System voted unanimously to

approve a 1/4 percentage point increase in the Primary Credit Rate to 5.5 percent, effective July 27, 2023."

In the action above, the Board approved requests to establish that rate submitted by the Boards of Directors of the Federal

Reserve Banks of Boston, Philadelphia, Cleveland, Richmond, Chicago, St. Louis. Minneapolis, Kansas City, Dallas, and

San Francisco.

approve a 1/4 percentage point increase in the Primary Credit Rate to 5.5 percent, effective July 27, 2023."

In the action above, the Board approved requests to establish that rate submitted by the Boards of Directors of the Federal

Reserve Banks of Boston, Philadelphia, Cleveland, Richmond, Chicago, St. Louis. Minneapolis, Kansas City, Dallas, and

San Francisco.

Within the first 24 seconds, Jerome Powell,

the Chairman of the Federal Reserve,

explainsthe difference between the Debt

and Deficit to Congressman John Kennedy

from Louisana, and then moves on to the

most important discussion of money -- M2.

the Chairman of the Federal Reserve,

explainsthe difference between the Debt

and Deficit to Congressman John Kennedy

from Louisana, and then moves on to the

most important discussion of money -- M2.

Interest Rate on Reserve Balances (IOR) is the MOST IMPORTANT TOOL OF MONETARY POLICY!

down

Students will NOT be tested on interest paid on Overnight Reverse Repurchase Agreement (ON RRP); however, they should

have the ability to marginally understand that the FED works with counter parties to increase or decrease reserves.

have the ability to marginally understand that the FED works with counter parties to increase or decrease reserves.

NIR

Primary credit is priced relative to the FOMC’s

target range for the federal funds rate and is

normally granted on a “no-questions-asked,”

minimally administered basis. There are no

restrictions on borrowers’ use of primary credit.

On March 15, 2020, the Federal Reserve announced

changes to primary credit. These changes included

the following:

Narrowing the spread of the primary credit rate

relative to the general level of overnight interest rates

to help encourage more active use of the window by

depository institutions to meet unexpected funding

needs.

Announcing that depository institutions may borrow

from the discount window for periods as long as 90

days, prepayable and renewable by the borrower on a

daily basis.

target range for the federal funds rate and is

normally granted on a “no-questions-asked,”

minimally administered basis. There are no

restrictions on borrowers’ use of primary credit.

On March 15, 2020, the Federal Reserve announced

changes to primary credit. These changes included

the following:

Narrowing the spread of the primary credit rate

relative to the general level of overnight interest rates

to help encourage more active use of the window by

depository institutions to meet unexpected funding

needs.

Announcing that depository institutions may borrow

from the discount window for periods as long as 90

days, prepayable and renewable by the borrower on a

daily basis.

Simple Review

The target range (lower limit) and target range (upper

limit) are NOT shown on the graph to the left.

The green line is the Federal Funds Rate which is the

POLICY RATE.

Administered Rate #1: The MOST IMPORTANT

administered tool of Monetary Policy is Interest paid on

Reserve Balances (IOR).

Administered Rate #2: Primary Credit Rate which is a

ceiling rate and is equal to the FOMC target range

upper limit.

Administered Rate #3: Interest paid on Overnight

Reverse Repurchase Agreements (ON RRP). Students

will NOT be tested on this concept in 2024.

The target range (lower limit) and target range (upper

limit) are NOT shown on the graph to the left.

The green line is the Federal Funds Rate which is the

POLICY RATE.

Administered Rate #1: The MOST IMPORTANT

administered tool of Monetary Policy is Interest paid on

Reserve Balances (IOR).

Administered Rate #2: Primary Credit Rate which is a

ceiling rate and is equal to the FOMC target range

upper limit.

Administered Rate #3: Interest paid on Overnight

Reverse Repurchase Agreements (ON RRP). Students

will NOT be tested on this concept in 2024.

| Expansionary Monetary Policy Flow Chart with REFF® AR GRAPH and ASAD GRAPH. |

| Required Reserves Rip It Out! Excess Reserves Rip It Out! Commercial Bank Balance Sheet Rip It Out! |

| Contractionary Monetary Policy Flow Chart with REFF® AR GRAPH and ASAD GRAPH. |

The Federal Reserve is the lender of last resort through the

Federal Reserve of New York's Discount Window:

The Primary Credit Rate, formerly called the Discount Rate

until 2003, serves as the principal safety valve for ensuring

adequate liquidity in the banking system. It is available to

depository institutions that are in generally sound financial

condition, and there are no restrictions on the use of funds

borrowed under primary credit.

Secondary Credit Rate is available to depository institutions

not eligible for primary credit. Secondary credit entails a higher

level of administration. In April of 2023, the Federal Reserve

stated the secondary credit rate would be 50 basis points

above the primary credit rate.

Seasonal Credit is available to assist small depository

institutions with demonstrated liquidity pressures of a

seasonal nature and will not normally be available to

institutions with deposits of $500 million or more. The

seasonal credit rate is reset every two weeks as the

average of the daily effective federal funds rate.

Federal Reserve of New York's Discount Window:

The Primary Credit Rate, formerly called the Discount Rate

until 2003, serves as the principal safety valve for ensuring

adequate liquidity in the banking system. It is available to

depository institutions that are in generally sound financial

condition, and there are no restrictions on the use of funds

borrowed under primary credit.

Secondary Credit Rate is available to depository institutions

not eligible for primary credit. Secondary credit entails a higher

level of administration. In April of 2023, the Federal Reserve

stated the secondary credit rate would be 50 basis points

above the primary credit rate.

Seasonal Credit is available to assist small depository

institutions with demonstrated liquidity pressures of a

seasonal nature and will not normally be available to

institutions with deposits of $500 million or more. The

seasonal credit rate is reset every two weeks as the

average of the daily effective federal funds rate.

| REFFONOMICS® BASEBALL -- Ample Reserves Regime |

| The FED starts paying Interest on required and excess reserves |

| Reffonomics.com Useful Links for Understanding Ample Reserves Regime |

| 2008 (October) |

| The "Discount Rate" is DISCONTINUED and replaced by the "Primary Credit Rate" |

| Expansionary Monetary Policy Flow Chart with REFF® AR GRAPH and ASAD GRAPH. |

| 2003 (January) |

| Contractionary Monetary Policy Flow Chart with REFF® AR GRAPH and ASAD GRAPH. |

| Expansionary Monetary Policy Flow Chart with REFF® AR GRAPH and ASAD GRAPH. |

| For AP® Macroeconomics Educators and Students: |

Below is a short video from The Dead Poets Society starring Robin Williams where he instructs his students

to rip out pages from their poetry book which should happen to many of the pages in economics textbooks

that relate to monetary policy of the past. Also, it is quite ironic that Robin Williams draws a graph about

poetry on the blackboard, as graphs tell important stories in economics.

to rip out pages from their poetry book which should happen to many of the pages in economics textbooks

that relate to monetary policy of the past. Also, it is quite ironic that Robin Williams draws a graph about

poetry on the blackboard, as graphs tell important stories in economics.

DO NOT USE THE TERM DISCOUNT RATE ANYMORE.

INSTEAD, USE THE TERM PRIMARY CREDIT RATE

THOUGH THE DISCOUNT WINDOW.

INSTEAD, USE THE TERM PRIMARY CREDIT RATE

THOUGH THE DISCOUNT WINDOW.

| The Past (10 minutes) |

| Ample Reserves Regime -- The Past, The Present, and The Future |

| September 19 - 20, 2023 FOMC Statement and Board of Governors' Press Release Lesson |

Every time you hear the terms Poem,

Poetry, or J. Evans Pritchard, say to

yourself -- OLD Monetary Policy.

Poetry, or J. Evans Pritchard, say to

yourself -- OLD Monetary Policy.

Before April 24, 2020, savings accounts were

not part of M1. Limitations in the number of

transfers from savings deposits made savings

accounts less liquid than M1. M1 consisted of

currency, demand deposits, and other highly

liquid accounts called “other checkable

deposits” (OCDs).

But the limitation on the number of these

transfers was lifted on April 24 as an

amendment to Regulation D, which specifies

how banks must classify deposit accounts.

Savings deposits are now just as liquid and

convenient as currency, demand deposits,

and OCDs.

not part of M1. Limitations in the number of

transfers from savings deposits made savings

accounts less liquid than M1. M1 consisted of

currency, demand deposits, and other highly

liquid accounts called “other checkable

deposits” (OCDs).

But the limitation on the number of these

transfers was lifted on April 24 as an

amendment to Regulation D, which specifies

how banks must classify deposit accounts.

Savings deposits are now just as liquid and

convenient as currency, demand deposits,

and OCDs.

A special thank you goes to The Council for Economics Education (CEE) for accepting my proposal to speak at the

62nd Financial Literacy & Economic Education Conference in Fort Lauderdale, Florida.

62nd Financial Literacy & Economic Education Conference in Fort Lauderdale, Florida.

| New Current Event Lessons Covering FOMC Meetings: |

| The FED starts paying INTEREST ON RESERVE BALANCES (IOR). This becomes the PRIMARY TOOL OF MONETARY POLICY. The FED, thus discontinues paying interest on required reserves (RR) and interest on ER on this date. |

| 2021 (August) |