| MACRO -- Unit 4, Topic 4.4 |

| Steven M. Reff Economics Lecturer University of Arizona (2007 - 2016) The 2015 University of Arizona Five-Star Faculty Award |

ESSENTIAL KNOWLEDGE

Depository institutions (such as commercial banks) organize their assets and liabilities on balance sheets.

(See Commercial Bank Balance Sheet below.)

Assets are what you own; liabilities are what you owe.

A commercial bank balance sheet has ASSETS of Required Reserves (RR), Excess Reserves (ER), and Loans

on the asset side of the balance sheet. Since the bank is in possession of these, they are part of the commercial

bank's ASSETS.

Descriptions of these ASSETS:

*Required Reserves (RR) is money that is held inside the commercial bank vault or on reserve with the

Federal Reserve (the U.S. central bank).

*Excess Reserves (ER) are those reserves that are left over after RR. These ER can be used in two main ways:

1) Make more loan. 2) Purchase government securities (bonds). Loans are the signed documents from the

borrowers that the bank has in its possession.

LIABILITIES--A commercial bank balance sheet has Demand Deposits and Owners' Equity:

Description of these LIABILITIES:

*Demand Deposits (DD), which are a nice way of saying checking accounts. Checks are considered to be

money and thus are payable on demand. This is the reason why checking account deposits are called Demand

Deposits. DD are placed on the liabilities side of the balance sheet because this is money in customers checking

accounts that is owed to them.

*Equity is what is owed to the investors or owners of the commercial bank.

Depository institutions operate using fractional reserve banking.

*The fractional reserve banking is a system in which only a fraction of bank deposits are required to be

available for withdrawal. The fraction of bank deposits are the Required Reserves (RR.)

Banks’ reserves are divided into required reserves and excess reserves.

*Banks must hold onto RR, but can use the ER for loans or purchasing bonds from the Federal Reserve (FED).

Depository institutions (such as commercial banks) organize their assets and liabilities on balance sheets.

(See Commercial Bank Balance Sheet below.)

Assets are what you own; liabilities are what you owe.

A commercial bank balance sheet has ASSETS of Required Reserves (RR), Excess Reserves (ER), and Loans

on the asset side of the balance sheet. Since the bank is in possession of these, they are part of the commercial

bank's ASSETS.

Descriptions of these ASSETS:

*Required Reserves (RR) is money that is held inside the commercial bank vault or on reserve with the

Federal Reserve (the U.S. central bank).

*Excess Reserves (ER) are those reserves that are left over after RR. These ER can be used in two main ways:

1) Make more loan. 2) Purchase government securities (bonds). Loans are the signed documents from the

borrowers that the bank has in its possession.

LIABILITIES--A commercial bank balance sheet has Demand Deposits and Owners' Equity:

Description of these LIABILITIES:

*Demand Deposits (DD), which are a nice way of saying checking accounts. Checks are considered to be

money and thus are payable on demand. This is the reason why checking account deposits are called Demand

Deposits. DD are placed on the liabilities side of the balance sheet because this is money in customers checking

accounts that is owed to them.

*Equity is what is owed to the investors or owners of the commercial bank.

Depository institutions operate using fractional reserve banking.

*The fractional reserve banking is a system in which only a fraction of bank deposits are required to be

available for withdrawal. The fraction of bank deposits are the Required Reserves (RR.)

Banks’ reserves are divided into required reserves and excess reserves.

*Banks must hold onto RR, but can use the ER for loans or purchasing bonds from the Federal Reserve (FED).

Excess reserves are the basis of expansion of the money supply by the banking system.

Banks CANNOT lend RR. Banks can only lend ER. These are total reserves minus RR.

The money multiplier is the ratio of the money supply to the monetary base.

Banks CANNOT lend RR. Banks can only lend ER. These are total reserves minus RR.

The money multiplier is the ratio of the money supply to the monetary base.

The amount predicted by the simple money multiplier may be overstated because it does not take into account

a bank’s desire to hold excess reserves or the public holding more currency.

Stated differently, if banks do not lend excess reserves or the public keeps more money,

then the money multiplier will not be as great--it is overstated.

a bank’s desire to hold excess reserves or the public holding more currency.

Stated differently, if banks do not lend excess reserves or the public keeps more money,

then the money multiplier will not be as great--it is overstated.

The video you will be watching is an allegory

of the Creation of Money written by

Professor Emeritus at the University of

Arizona, Don Wells.

Don passed away in June 2022 at

the age of 92, but his story lives on

in the annals of teaching the Creation of

Money and a Commerical Bank's Balance

Sheet.

While you are watching this 32-minute video,

you will get to a part in the video about

a Bank's Balance Sheet. Keep glancing at the

Balance Sheet above the video.

It is REQUIRED on the May exam.

of the Creation of Money written by

Professor Emeritus at the University of

Arizona, Don Wells.

Don passed away in June 2022 at

the age of 92, but his story lives on

in the annals of teaching the Creation of

Money and a Commerical Bank's Balance

Sheet.

While you are watching this 32-minute video,

you will get to a part in the video about

a Bank's Balance Sheet. Keep glancing at the

Balance Sheet above the video.

It is REQUIRED on the May exam.

Knowledge of the Balance Sheet of a Commercial Bank

to the left is REQUIRED for the May Exam!

Your knowledge of Topics 4.4 and 4.5 are your

responsibility since these are history lessons about how

monetary policy was initiated in the past. You will be

learning about these topics through online homework

assignments from this website. You will learn about

how today's Monetary Policy is initiated inside the

classroom when Topic 4.6 is taught.

to the left is REQUIRED for the May Exam!

Your knowledge of Topics 4.4 and 4.5 are your

responsibility since these are history lessons about how

monetary policy was initiated in the past. You will be

learning about these topics through online homework

assignments from this website. You will learn about

how today's Monetary Policy is initiated inside the

classroom when Topic 4.6 is taught.

The size of expansion of the money supply depends on the money multiplier.

The formula for the money multiplier is easy.

It is 1/r or 1 divided by the Reserve Ratio.

The maximum value of the money multiplier can be calculated as the reciprocal

of the required reserve ratio.

If a bank has $1 million in DD (demand deposits) and $200,000 in required reserves,

the reserve ratio is equal to 1/5. The reciprocal of this reserve ratio is equal to 5.

$200,000/$1,000,000 = 1/5 so the money multiplier is equal to 5.

The formula for the money multiplier is easy.

It is 1/r or 1 divided by the Reserve Ratio.

The maximum value of the money multiplier can be calculated as the reciprocal

of the required reserve ratio.

If a bank has $1 million in DD (demand deposits) and $200,000 in required reserves,

the reserve ratio is equal to 1/5. The reciprocal of this reserve ratio is equal to 5.

$200,000/$1,000,000 = 1/5 so the money multiplier is equal to 5.

Money Multiplier =

Change in the Money Supply (MS) divided by

the Change in the Monetary Base (MB or M0)

the Change in the Monetary Base (MB or M0)

| HOMEWORK ASSIGNMENTS for Part II |

| eVideos with 3 multiple-choice questions located below the video: |

Simple Money Multiplier, Part I:

https://reffonomics.com/12ASimpleMoneyMultiplierPartIB.html

Simple Money Multiplier, Part II:

https://reffonomics.com/12ASimpleMoneyMultiplierPartIIB.html

https://reffonomics.com/12ASimpleMoneyMultiplierPartIB.html

Simple Money Multiplier, Part II:

https://reffonomics.com/12ASimpleMoneyMultiplierPartIIB.html

| eVideos with 3 multiple choice questions underneath the video: |

Reserve Requirement (2:50 minutes)

https://reffonomics.com/12ReserveRequirementBalanceSheetB.html

Discount Rate (3:12 minutes)

https://reffonomics.com/12ADiscountRateBalanceSheetB.html

Open-Market Operations (3:07 minutes)

https://reffonomics.com/12AOpenMarketOperationsBalanceSheetB.html

https://reffonomics.com/12ReserveRequirementBalanceSheetB.html

Discount Rate (3:12 minutes)

https://reffonomics.com/12ADiscountRateBalanceSheetB.html

Open-Market Operations (3:07 minutes)

https://reffonomics.com/12AOpenMarketOperationsBalanceSheetB.html

| HOMEWORK ASSIGNMENTS for Part I: |

| eVideo (an allegory about the Creation of Money) for Topic 4.4 (32 minutes) |

| eTextbook Readings for Topic 4.4: |

History of the Reserve Requirement and the Discount Rate:

https://reffonomics.com/FederalReserveTools2BRAeconomics2021.html

https://reffonomics.com/FederalReserveTools2BRAeconomics2021.html

History of Open-Market Operations:

https://reffonomics.com/FederalReserveTools3BRAeconomics2021.html

https://reffonomics.com/FederalReserveTools3BRAeconomics2021.html

| TOPIC 4.4, Part I: BANKING AND THE EXPANSION OF THE MONEY SUPPLY |

| TOPIC 4.4, Part II: BANKING AND THE EXPANSION OF THE MONEY SUPPLY |

- - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - -

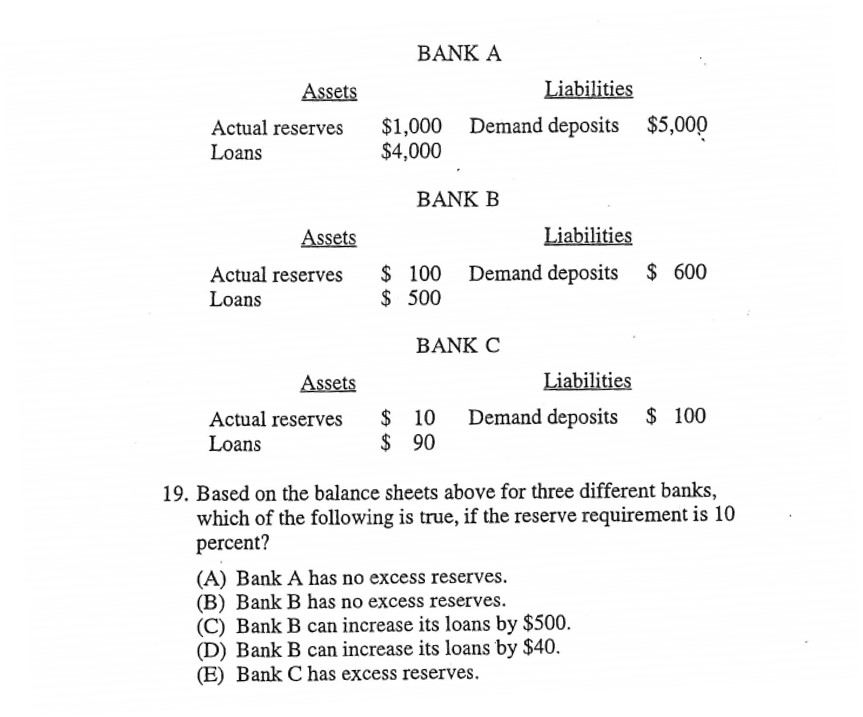

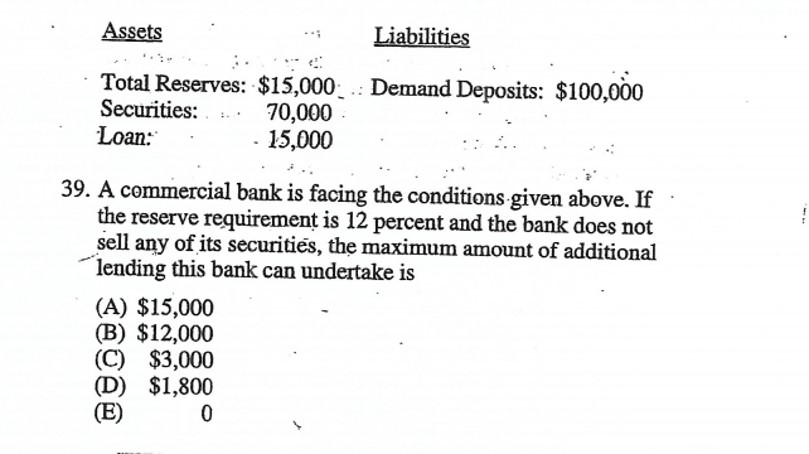

Located below are two sample multiple choice questions that will be similar to questions you might see on your May exam. Actual Reserves and Total Reserves includes BOTH

REQUIRED RESERVES and EXCESS RESERVES.

REQUIRED RESERVES and EXCESS RESERVES.

The History of Monetary Policy will be the students' responsibility to learn in this homework

assignment on Topic 4.4 -- Banking and the Expansion of the Money Supply and in the next

homework assignment on Topic 4.5 The Money Market.

assignment on Topic 4.4 -- Banking and the Expansion of the Money Supply and in the next

homework assignment on Topic 4.5 The Money Market.